Financial Corner: Education Tax Credits and Deductions

Editor's Note: This content is sponsored by Aegis Capital

By Aegis Capital

Feb. 4, 2026: For parents and students trying to manage college bills and student loan payments, the federal government offers education-related tax benefits. The requirements for each are different, so here's what you need to know.

American Opportunity Credit

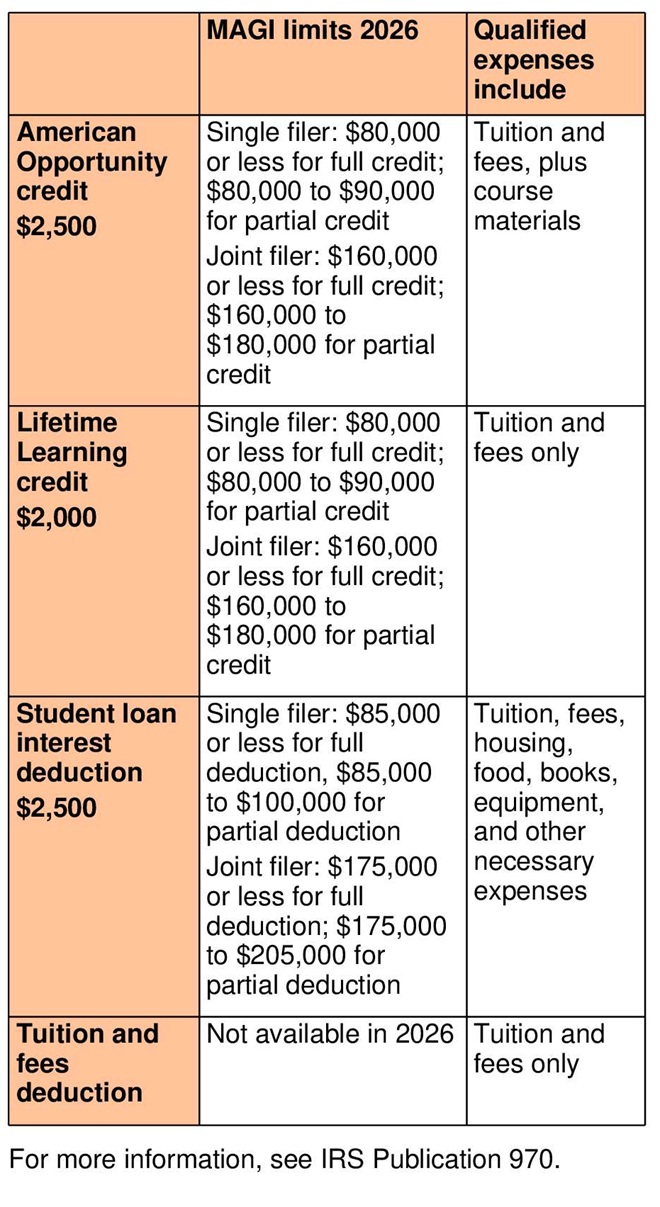

The American Opportunity credit (formerly the Hope credit) is a tax credit available for the first four years of a student's undergraduate education, provided the student is attending school at least half-time in a program leading to a degree or certificate. The credit is worth up to $2,500 in 2026 (it's calculated as 100% of the first $2,000 of qualified expenses plus 25% of the next $2,000 of expenses). The credit must be taken for the tax year that the expenses are paid, and parents must claim their child as a dependent on their tax return to take the credit.

To be eligible for the credit, your income must fall below certain limits. In 2026, a full credit is available to single filers with a modified adjusted gross income (MAGI) below $80,000 and joint filers with a MAGI below $160,000. A partial credit is available to single filers with a MAGI between $80,000 and $90,000 and joint filers with a MAGI between $160,000 and $180,000.

One benefit of the American Opportunity credit is that it's calculated per student, not per tax return. So parents with two (or more) qualifying children in a given year can claim a separate credit for each child (assuming income limits are met).

The mechanics of claiming the credit are relatively easy. If you paid tuition and related expenses to an eligible educational institution during the year, the college generally must send you a Form 1098-T by February 1 of the following year. You then file Form 8863 with your federal tax return to claim the credit.

Lifetime Learning Credit

The Lifetime Learning credit is another education tax credit, but it has a broader reach than the American Opportunity credit. As the name implies, the Lifetime Learning credit is available for college or graduate courses taken throughout your lifetime (the student can be you, your spouse, or your dependents), even if those courses are taken on a less than half-time basis and don't lead to a formal degree. This credit can't be taken in the same year as the American Opportunity credit on behalf of the same student.

The Lifetime Learning credit is worth up to $2,000 in 2026 (it's calculated as 20% of the first $10,000 of qualified expenses). The Lifetime Learning credit must be taken for the same year that expenses are paid, and you must file Form 8863 with your federal tax return to claim the credit. In 2026, a full credit is available to single filers with a modified adjusted gross income (MAGI) below $80,000 and joint filers with a MAGI below $160,000. A partial credit is available to single filers with a MAGI between $80,000 and $90,000 and joint filers with a MAGI between $160,000 and $180,000.

Unlike the American Opportunity credit, the Lifetime Learning credit is limited to $2,000 per tax return per year, even if more than one person in your household qualifies independently in a given year.

If you have more than one family member attending college or taking courses at the same time, you'll need to decide which credit to take.

Example: Joe and Ann have a college freshman and sophomore, Mary and Ben, who are attending school full-time. In addition, Joe is enrolled at a local community college taking two graduate courses related to his job. Mary and Ben each qualify for the American Opportunity credit. Plus, Mary, Ben, and Joe each qualify for the Lifetime Learning credit. Because the American Opportunity credit isn't limited to one per tax return, Joe and Ann should claim this credit for both Mary and Ben, and then claim a Lifetime Learning credit for Joe. Joe and Ann can claim both the American Opportunity credit and the Lifetime Learning credit in the same year because each credit is taken on behalf of a different qualified student.

Student Loan Interest Deduction

Comparison of Credits/Deductions The student loan interest deduction allows borrowers to deduct up to $2,500 worth of interest paid on qualified student loans in 2026. Generally, federal student loans, private bank loans, college loans, and state loans are eligible. However, the debt must have been incurred while the student was attending school on at least a half-time basis in a program leading to a degree, certificate, or other recognized educational credential. So loans obtained to take courses that do not lead to a degree or other educational credential are not eligible for this deduction.

Your ability to take the student loan interest deduction depends on your income. For 2026, to take the full $2,500 deduction (assuming that much interest is paid during the year) single filers must have a MAGI of $85,000 or less and joint filers $175,000 or less. A partial deduction is available for single filers with a MAGI between $85,000 and $100,000 and joint filers with a MAGI between $175,000 and $205,000.

Also, to be eligible for the deduction, an individual must have the primary obligation to pay the loan and must pay the interest during the tax year. The deduction may not be claimed by someone who can be claimed as a dependent on another taxpayer's return. Borrowers can take the student loan interest deduction in the same year as the American Opportunity credit or Lifetime Learning credit, provided they qualify for each independently.

Tuition and Fees Deduction

The deduction for tuition and fees is not available in 2026. It was last available in 2020, when it was worth up to $4,000 for out-of-pocket qualified tuition and fee expenses paid during the year. Single filers with a modified gross income (MAGI) of $65,000 or less and joint filers with a MAGI of $130,000 or less could take the full $4,000 deduction. A $2,000 partial deduction was available for single filers with a MAGI between $65,000 and $80,000 and joint filers with a MAGI between $130,000 and $160,000.

Comparison of Credits/Deductions

IMPORTANT DISCLOSURES Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, legal, or retirement advice or recommendations. The information presented here is not specific to any individual's personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable — we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice

Aegis Capital Corp.

Steve & Jane Ircha & Richard Palmadesso

Pictured: Steve & Jane Ircha

Steven Ircha Senior Managing Director 26 Paxton Ave. 914-361-1099 This email address is being protected from spambots. You need JavaScript enabled to view it. https://www.ircha.com

Financial & Legal Assistance Directory

Hymes & Associates, CPA, P.C.

Our firm provides outstanding service to our clients because of our dedication to the three underlying principles of professionalism, responsiveness, and quality.

Listed as one of the 10 largest firms by The Westchester Business Journal, we serve clients throughout the tri-state area. By combining our expertise, experience, and

the energy of our staff, each client receives close, personal and professional attention.

Our high standards, service, and specialized staff spell the difference between our outstanding performance and other firms. We make sure that every client

is served by the expertise of our whole firm.

Hymes & Associates, CPA, P.C.

55 Pondfield Road

Bronxville, NY 10708

914-961-1200

914-961-1715 (Fax)

Website: www.hymescpa.com

Baillie & Hershman

44 Pondfield Road, Suite - 12

Bronxville, N.Y. 10708

Office: 914-337-6300

Matthew W. Kerner, ESQ.

Direct Dial: 914-337-6569

Email: This email address is being protected from spambots. You need JavaScript enabled to view it.

Fax: 914-337-6913

Suzanne M. Bloomer, Esq.

Direct Dial: 914-337-0142

This email address is being protected from spambots. You need JavaScript enabled to view it.

Baillie & Hershman provides comprehensive Real Estate legal services for buyers, sellers, current owners, real estate agents and lenders. We also handle estate planning, including the drafting of wills.

Griffin, Coogan, Sulzer & Horgan, P.C.

Attorneys and Counselors at Law

Griffin, Googan, Sulzer & Horgan, R.C.

Located in Bronxville, New York, Griffin, Coogan, Sulzer & Horgan, P.C. takes great pride in providing our clients with comprehensive, high quality legal services in a responsive manner. The firm concentrates its practice in real estate law with a primary focus on issues relating to real estate tax litigation (also known as tax certiorari), real estate transactions, valuation law, real property taxation and tax planning and real property tax exemption matters throughout New York State.

The firm serves as general counsel for several local cooperatives and represents clients in various issues relating to wills, trusts and estate planning.

51 Pondfield Road

Bronxville, NY 10708

(914) 961-1300

This email address is being protected from spambots. You need JavaScript enabled to view it.

Nobile, Magarian & DiSalvo LLP

We are hardworking and dedicated attorneys who, combined, have more than 150 years of experience delivering quality legal advice. Our cutting edge is our ability to enter both the conference room and the courtroom with strength. Our law firm provides legal representation and counsel for both individual and business clients on issues related to estate planning and administration, real estate law, litigation, and business law. Our practice areas include: Commercial Litigation, Business Law, Real Estate, Wills, Estate Planning, Trusts, Estate Administration, Living Wills, Health Care Proxies, Powers of Attorney, Not For Profits, and Employment Law.

111 Kraft Avenue

Bronxville, NY 10708

914-337-6300

Veneruso, Curto, Schwartz & Curto, LLP

Veneruso, Curto, Schwartz & Curto is dedicated to providing businesses and individuals with exceptional legal services customized to each client's needs and objectives. Practice areas include litigation, real estate, not for profit, wills and estate planning, land use and zoning, business and corporate, cooperative and condominium and real estate tax assessment litigation.

The Hudson Valley Bank Building

35 East Grassy Sprain Road, Suite 400

Yonkers, New York 10710

914-779-1100

Aegis Capital

Steve brings 40 years of investing experience to his role as Senior Managing Director at Aegis Capital Corp., a prominent national securities firm.

Financial Legal Assistance Recent Articles

Quick Links

Newsletter

MyhometownBroxnville reserves the right to monitor and remove all comments. For more information on Posting Rules, please review our Rules and Terms of Use, both of which govern the use and access of this site. Thank you.

The information presented here is for informational purposes only. While every effort has been made to present accurate information, myhometownBronxville, LLC, does not in any way accept responsibility for the accuracy of or consequences from the use of this information herein. We urge all users to independently confirm any information provided herein and consult with an appropriate professional concerning any material issue of fact or law. The views and opinions expressed by the writers, event organizers and advertisers do not necessarily represent those of myhometownBronxville, LLC, its officers, staff or contributors. The use of this website is governed by the Terms of Use . No portion of this publication may be reproduced or redistributed, either in whole or part, without the express written consent of the publisher.

Copyright © 2009 myhometownbronxville.com, All rights reserved.